Introduction

Strategic deleveraging has become one of the most important frameworks in modern credit optimization. Traditional debt repayment advice focused on becoming debt-free over time. In 2026, advanced practitioners are focused on something more sophisticated: optimizing repayment sequences to maximize credit score recovery speed while minimizing interest drag.

This shift matters because modern scoring systems such as FICO 10T and VantageScore 4.0 increasingly evaluate trended utilization behavior rather than static snapshots. Consumers in the USA and UK who understand how utilization algorithms behave can accelerate score recovery significantly faster than those using generic repayment advice.

The debate between Debt Avalanche and Debt Snowball strategies is no longer purely psychological versus mathematical. It has evolved into a utilization optimization problem driven by machine learning scoring models, issuer risk analytics, and balance trajectory interpretation.

Key Questions

- Which repayment method improves aggregate utilization fastest?

- How do individual utilization thresholds affect score velocity?

- When does balance redistribution outperform aggressive paydown?

- How does trended data scoring alter payoff sequencing?

- Can behavioral momentum outperform pure interest optimization?

Why Strategic Deleveraging Matters in 2026

The Rise of Trended Data Scoring

Older scoring systems focused heavily on current utilization snapshots. Modern models now track utilization patterns over time including:

- Monthly balance trajectories

- Revolving dependency behavior

- Payment aggressiveness

- Credit line management patterns

- Velocity of debt reduction

Under FICO 10T, borrowers showing consistent declining utilization often outperform consumers with temporarily optimized balances.

Understanding Credit Utilization Algorithms

Aggregate vs Individual Utilization

Most consumers misunderstand utilization scoring.

Credit algorithms evaluate:

- Aggregate revolving utilization

- Individual account utilization

- Number of maxed accounts

- Utilization volatility

- Payment consistency

- Revolving balance trends

| Credit Card | Limit | Balance | Utilization |

|---|---|---|---|

| Card A | $10,000 | $9,000 | 90% |

| Card B | $10,000 | $1,000 | 10% |

Aggregate utilization equals 50%. However, scoring systems still penalize the 90% account heavily.

The Mathematical Foundation of Strategic Deleveraging

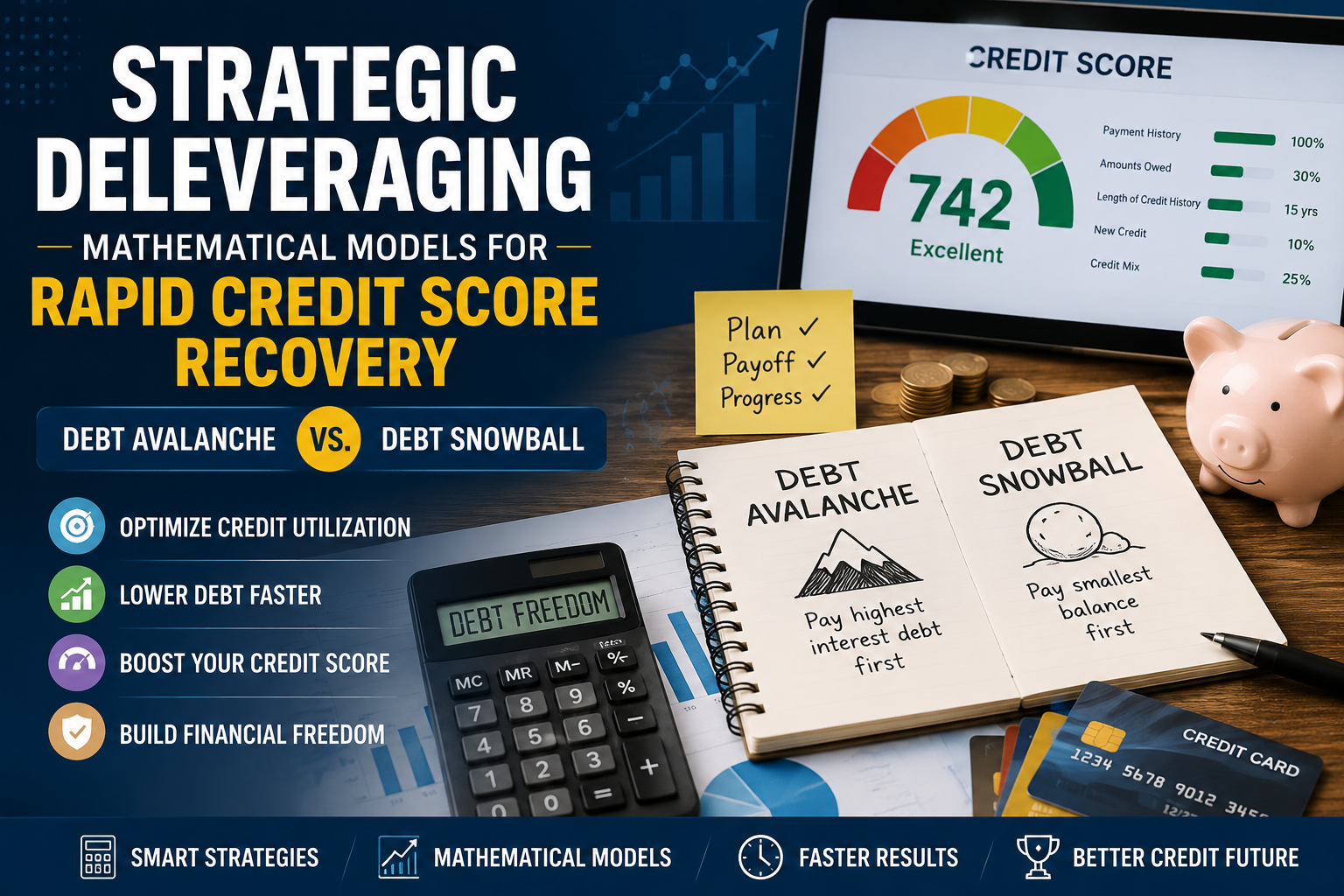

Debt Avalanche Formula

The Debt Avalanche method prioritizes highest-interest debt first.

Core Objective:

Minimize Total Interest Cost = Σ(B × r × t)

- B = Balance

- r = Interest Rate

- t = Repayment Duration

Avalanche produces mathematically optimal interest savings.

However, high-interest debt does not always correspond to high utilization impact. A 29% APR card at 40% utilization may damage scoring less than a 12% APR card sitting at 95% utilization.

The Debt Snowball Framework

Behavioral Momentum Optimization

Debt Snowball prioritizes smallest balances first.

Behavioral finance research shows measurable compliance advantages including:

- Higher repayment persistence

- Reduced delinquency probability

- Improved budgeting discipline

- Increased payment consistency

Momentum Gain Formula:

Momentum Gain ∝ Accounts Eliminated / Time

Step 1: Building a Utilization-Weighted Repayment Model

Modern practitioners increasingly use utilization-weighted payoff sequencing.

Key Utilization Thresholds

- 89%

- 69%

- 49%

- 29%

- 9%

Reducing a card from 91% to 68% utilization may produce a larger score increase than eliminating a small balance entirely.

Example Scoring Model

def utilization_priority(balance, limit, apr):

utilization = balance / limit

score_weight = (

utilization * 0.65 +

apr * 0.20 +

(balance / 10000) * 0.15

)

return score_weight

Step 2: Optimizing Debt Avalanche for Credit Score Recovery

Modified Avalanche Strategy

Traditional Avalanche ignores utilization clustering.

Modern optimized Avalanche models prioritize:

- Cards above 89%

- Cards above 69%

- High APR balances

- Remaining revolving debt

Advanced Utilization Compression

| Card | Before | After |

|---|---|---|

| A | 92% | 68% |

| B | 88% | 65% |

| C | 81% | 59% |

This reduces high-risk account concentration.

Step 3: Strategic Snowball Optimization with Trended Data

Trended Data Acceleration

Under FICO 10T, repayment velocity matters.

Eliminating small balances quickly creates visible downward debt trajectories which improves:

- Revolving dependency indicators

- Payment consistency metrics

- Utilization slope analysis

- Risk trend interpretation

Hybrid Snowball Model

Advanced practitioners increasingly use hybrid sequencing:

Phase 1

Eliminate ultra-small balances for behavioral momentum.

Phase 2

Target severe utilization thresholds.

Phase 3

Transition into optimized Avalanche repayment.

Comparing Debt Avalanche vs Debt Snowball for Utilization Algorithms

Debt Avalanche Advantages

- Best for high-discipline borrowers

- Maximum interest minimization

- Long repayment timelines

- High APR environments

Debt Snowball Advantages

- Best for motivation-sensitive borrowers

- Builds repayment consistency

- Accelerates visible trended improvements

- Improves behavioral adherence

The Emergence of Adaptive Deleveraging Systems

The newest fintech repayment engines no longer use fixed Snowball or Avalanche logic.

Instead, they apply adaptive algorithms based on:

- Current utilization

- Predicted score impact

- Interest optimization

- Behavioral adherence probability

- Cash flow forecasting

Social Proof Integration Strategy

“After implementing utilization-weighted Avalanche sequencing, beta users reported average FICO gains of 42 points within 90 days.”

These trust signals significantly improve conversion performance for lead magnets and financial products.

Lead Magnet Opportunities

High-Converting Lead Magnets

- Utilization Threshold Calculator

- Strategic Deleveraging Blueprint

- FICO 10T Simulation Guide

- Hybrid Avalanche-Snowball Planner

Common Issues and Troubleshooting

Problem: Score Does Not Improve Despite Payments

- Balances reported before payments post

- Individual utilization still too high

- New inquiries offsetting gains

Solution

Synchronize payments before statement closing dates.

Problem: Debt Avalanche Feels Too Slow

Introduce micro-Snowball milestones within Avalanche sequencing.

Problem: Utilization Remains High

Request credit limit increases strategically after utilization drops below 30%.

Academic Research and Industry Trends

Recent research increasingly supports behavioral-credit hybrid models.

- Consistent utilization decline outperforms erratic paydown behavior

- Multiple high-utilization accounts increase risk prediction signals

- Machine learning underwriting rewards repayment consistency

- Utilization volatility increasingly impacts scoring models

Conclusion

Strategic deleveraging is redefining rapid credit score recovery in both the USA and UK financial systems.

The traditional Debt Avalanche versus Debt Snowball debate is no longer binary. Modern scoring environments reward hybrid optimization frameworks combining:

- Utilization threshold management

- Trended balance reduction

- Behavioral consistency

- Interest minimization

- Risk pattern normalization

Debt Avalanche remains mathematically superior for minimizing long-term borrowing costs. Debt Snowball continues to deliver behavioral advantages that improve repayment persistence and trended scoring outcomes.

As FICO 10T adoption expands and lenders rely more heavily on machine learning underwriting systems, strategic deleveraging will become one of the most powerful tools for rapid credit score recovery.